Over the past two years there has been an orgy of finger-pointing about who’s to blame for the Great Recession. It was the nefarious bankers who piled up excessive leverage on their balance-sheets. It was irresponsible mortgage lenders in the United States who lent to borrowers clearly unable to repay their loans (sub-prime mortgages) – or to the irresponsible borrowers themselves. Regulators have come in for a lashing because they were seen to be asleep at the switch; and politicians for the deregulatory craze that started decades before and led first to the Big Bang in London in 1986 and then the repeal of the 1933 Glass-Steagall Act in the United States under President Clinton. The mortgage firms Fannie Mae and Freddie Mac have been blamed for allowing US mortgage lending standards to decline, and Alan Greenspan, former Chairman of the Fed, has taken a knock for excessively lax monetary policy in the first decade of this century. Even past US presidents (Bill Clinton, George W. Bush) have not been spared for their policies promoting the American Dream of universal home ownership for all households, a dream that we now know was unrealistic.

Some people want to sweep even wider in their condemnation. François Hollande, the presidential candidate of the Socialist Party in France, considers that it is the entire world of finance in the widest sense that is to blame ("Mon véritable adversaire c’est le monde de la finance"). The "Occupy Wall Street" movement has channeled legitimate anger about the loss of livelihoods, rise in unemployment and worsening economic conditions in the US into an inchoate anger against the eponymous New York neighborhood. At a time of worsening wealth and income equality, the "one percent" of wealthiest individuals is now considered legitimate prey for public anger.

There is no doubt that over the past decade there has been some breathtakingly irresponsible behavior in the economic spheres of the United States and Europe. All of the proximate causes of the Great Recession listed above are to some extent valid. It’s difficult not to feel that the financial sector in its broadest sense has let the world down badly, and we are all paying for their wild partying. And they do not even seem to feel repentant; even during the height of the crisis bankers continued to receive lavish bonuses. M. Hollande is expressing a sentiment widely felt and richly deserved.

However, economists are increasingly stepping back and looking at the longer term trends, to try to understand the deep-seated forces at play. More than just bankers’ cupidity seems at work. They have gone back to study former financial crises 1 , and been reviewing the changes that have occurred in the global financial system over past decades. Philip Coggan, a former journalist at both the Financial Times of London and The Economist, has just published an entertaining but sobering review of these changes in a book entitled “Paper Promises’. 2 In particular, he has highlighted the staggering explosion of debt, both private and public, that has occurred over the past forty years.

The gold standard, the Bretton Woods System and “Tricky Dickey’ 3

Up until the beginning of the First World War the global financial system had been largely based on the gold standard, and the financial stability that ensued in the latter half of the Nineteenth Century led to stable growth and economic globalization. The First World War put an end to that, and the interwar period was marked by financial and economic turmoil. Attempts to return to the gold standard following the war were met for the most part with disastrous results. 4 In the UK for example, returning to the standard at the pre-war exchange rate led to a deep depression and ultimately to Britain leaving the standard. 5 The fragile Weimar Republic went through a hyper-inflationary phase by printing money rather than deal with the persistent budget deficit brought on by the need to pay Allied reparations. By the end of 1923, a kilo of butter cost 250 billion marks. 6 Around this time my grandfather, a British army officer stationed with the Allied occupation forces in Berlin after the First World War, bought a second-hand Bösendorfer piano for £10. (Sterling, still backed by gold at that time, was real money in those days.) In the US, after a stock market bubble in the late 1920s the country went into deep depression in the 1930s with unemployment reaching 25%, largely due to misguided monetary and fiscal policies. Worldwide trade dropped by 50% in the 1930s. It was a grim time and eventually led to even worse.

At the end of the Second World War world leaders in the industrialized countries took stock of the interwar turmoil and felt that the world needed to return to a global currency system of stable exchange rates and open trade. In 1944 at the Bretton Woods conference in New Hampshire they adopted a system of fixed exchange rates linked to the dollar, which was itself backed by gold at a price fixed at $35 per ounce. The Bretton Woods institutions were created 7 , including the International Monetary Fund to help countries deal with temporary imbalances in their balance of payments.

For quarter of a century following the Second World War the Bretton Woods system worked well, delivering high economic growth with low unemployment. It coincided with – and perhaps caused – the Japanese postwar economic miracle, the German Wirtschaftswunder and les trentes glorieuses in France. 8 At the same time industrialized economies were also extending retirement and other welfare systems to their populations, who in some cases (such as France) were newly urbanizing with a post-war migration out of rural areas. The high economic growth rates of the time, in addition to the favorable age pyramid (with many workers for each beneficiary) and relatively short life expectancy made such systems affordable during the first three decades. However, their introduction has come to represent very significant contingent liabilities for governments in today’s era of low growth, aging populations and longer lives.

Ultimately the Bretton Woods system’s fixed exchange rates did not adjust enough to account for divergent growth paths between the different countries, notably with the US which played the linchpin position, and the US budget and trade deficits brought on by the expansion of the Vietnam War let to a precipitous decline in US stocks of gold. In August 1971 things became untenable, and President Nixon had to choose between increasing interest rates to attract capital, which would have precipitated a recession in the United States, or suspend the convertibility of the dollar to gold. He chose the latter path.

A new regime of floating rates

To everyone’s surprise, the world did not come to an end when the US left the gold standard. The fact that the US dollar could no longer be converted into gold at a rate of $35 per ounce did not seem to make much of a difference to anyone, at least at first. However, within a few years a number of external events like the 1973 Arab-Israeli War and the resulting hike in crude oil prices, set the world on a whirlwind of stagflation – a combination of economic stagnation and inflation, high unemployment and rising prices at the same time. Conventional Keynesian economic thinking had difficulty explaining how the two could coexist. It was only after savage monetary tightening (the US prime rate peaked at an all-time record of 21.5 percent in December 1980) that inflation was finally licked in the rich countries. At least it seemed that way.

Blowing bubbles

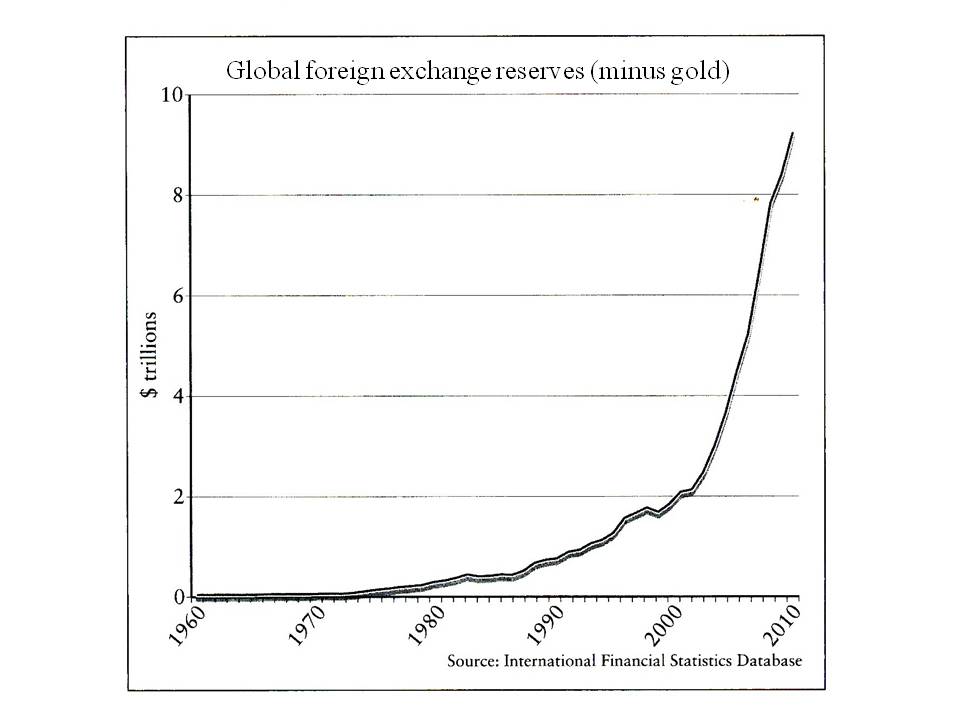

In retrospect, the departure from the Bretton Woods system unleashed an explosion of worldwide credit – and the opposite side of the coin, the ramping up of worldwide debt. Unraveling Bretton Woods had a direct effect on foreign exchange reserves – one country’s financial claims on another – which grew from an effective level of close to zero during the Bretton Woods years (all foreign reserves were then in dollars backed by gold, or for the US, in gold), to reach around $1 trillion in 1990 and more than 9 trillion in 2010.

International Financial Statistics Database

The more than fourfold growth in worldwide foreign exchange reserves over the past ten years is far higher than the growth of world GDP over the same period. This imbalance between creditor and debtor nations is one of the consequences of the explosion of credit that occurred once central bankers and the financial system were no longer confined to the Bretton Woods monetary straitjacket.

This period also coincided with a slow-down in economic growth and drop in birth-rate that transformed the generous but affordable welfare packages of the 1950s into major drains on the public purse in the 1990s and 2000s. Governments have often preferred to pay for these systems through borrowing rather than increases in taxes, especially following the war on taxes introduced by President Reagan and by Margaret Thatcher in the 1980s. It has always been easier to cut taxes than to cut welfare benefits.

In the private sphere, financial products such as credit cards – as sources of lending rather than payment, home equity lines of credit, and interest-only mortgages were now being marketed to consumers by a newly vitalized financial sector. The bond market, which in the 1960s had been directed solely to sovereign and municipal lenders, now discovered lending to corporates and exploded in volume. During the Bretton Woods period banking had been a rather boring business, akin to a utility. Now banking became the haven of high fliers and rocket scientists, attracted by the highly attractive compensation.

Growth in credit essentially means creation of money. But after the inflationary period of the late 1970s, growth in money supply at rates higher than GDP did not result in fresh inflation, at least as measured by increases in the prices of consumer items in rich countries. Rather, a series of financial imbalances started to manifest themselves: excessive lending to Latin American countries which caused a debt crisis of the early 1980s, the Asian financial crisis of 1997, a default by Russia on its bonds in 1998, the dot.com bubble in tech stocks which burst in 2000, and the housing bubble that culminated in the financial crisis of 2008. In Europe, growth in credit led to untenable sovereign debt borrowing by countries like Greece, Portugal and Italy, especially after the introduction of the Euro and convergence of Eurozone interest rates.

Arguably, the new floating exchange rate system has had some real benefits for the world economy also. The opening up of international capital markets has been a huge boon for developing countries, which have been able to access financial resources for their economic development. Such resources have not always been wisely invested but for the most part they have led to dramatically better endowments of infrastructure and productive and human capital which have given us the emerging economic powerhouses of today. Open financial markets and international trade have done more for economic development than all the aid agencies of the rich countries put together.

Tethering currencies to gold made no sense 9 – but untethering them in the 1970s let loose a demon of unstoppable credit creation and a wild fairground ride of debt-induced bubbles based on inflation of assets. The genie is out of the bottle, and no-one can put it back in.

How will it all end?

Debt, by its nature, pits creditors against debtors, owners of financial resources against those who lack them. This economic divide is much more significant than a Marxist Labor-versus-Capital distinction because it brings into play an important demographic dimension. Economic agents who are “long’ in financial resources tend to be in the latter part of their lives after decades of saving and investing, whereas the indebted are often starting out in life. So the debt divide becomes a generational distinction. Moreover, history tells us that untenable debt seldom gets paid back.

Ultimately, that is what I believe is the likely outcome for the huge public and private debt burdens that have built up over the past forty years – they will not be paid back in whole. The only thing that needs to be worked out is whether the default on this mountain of debt is through explicit repudiation by borrowers, through inflation, or both.

-

The most notable is: Reinhart, Carmen M. & Rogoff Kenneth S., This Time Is Different: Eight Centuries of Financial Folly, Princeton NJ, Princeton University Press, 2009. ↩

-

Coggan, Philip, Paper Promises – Debt, Money and the New World Order, New York, Public Affairs, 2012. ↩

-

President Richard Nixon. ↩

-

France is the one exception. ↩

-

The UK was running a trade deficit and the bulk of the gold that before the war had been in British coffers was now in the US. ↩

-

The world would not encounter such hyperinflation again until Hungary in 1947, Brazil in the late 1980s, and Zimbabwe in the latter years of the last decade. In Zimbabwe, after a reconversion of one trillion to one in 2009, the country has effectively abandoned its currency and uses the South African Rand. ↩

-

The International Monetary Fund, the World Bank and the General Agreement on Trade and Tariffs (GATT), transformed in 1995 into the World Trade Organization. ↩

-

Some economists argue that the introduction at this time of mandatory secondary schooling in Europe and Japan contributed very significantly, perhaps more than the introduction of the Bretton Woods system, by increasing labor productivity. ↩

-

The supply of gold does not follow world GDP growth patterns, so tying currencies to gold will induce monetary loosening or tightening depending on worldwide gold supply rather than on requirements of the economy. The chief advantage of the gold standard is that it removes monetary policy from the hands of politicians. ↩